Appalachian natural gas producers and marketers are adapting to a new status quo — a world where new pipeline takeaway capacity out of the Northeast is hard to come by and is more or less capped ad infinitum. Without the assurance of pipeline expansions, regional gas producers are no longer drilling with abandon in hopes that the capacity will eventually get built. Instead, producers are practicing restraint by slowing drilling activity, delaying completions and choking back producing wells to manage their inventory during periods of lower demand and prices. In today’s RBN blog, we consider what this new playbook will mean for pricing trends in the supply basin.

Pipeline constraints are nothing new for Appalachian gas producers. Over the past decade, Appalachian natural gas production (blue line in Figure 1) rocketed up to more than 35 Bcf/d, often straining infrastructure and pummeling local price basis — at least until the next tranche of pipeline capacity came online. In recent years, however, Appalachian gas producers have settled into maintenance mode, keeping production relatively flat, even in 2022, despite Russia’s invasion of Ukraine, the resulting energy security crisis, and low storage inventories sending supply basin gas prices rocketing to $9/MMBtu, the highest in over a decade. Among the pressures keeping production flat, producers have battled a number of headwinds since the pandemic, from inflation to shortages of materials and labor, along with hedges entered in late 2020 and 2021 that didn’t allow them to immediately benefit from the lofty gas prices seen last year. However, far and away the biggest constraint for Appalachian producers has been the increasingly grim prospects for new pipeline takeaway capacity.

Figure 1. Northeast Natural Gas Production Receipts vs. Deliveries. Source: Wood Mackenzie flow data[url=https://footprosports.com/

If we look at Northeast production and demand going back to 2010 based on interstate pipeline flow data from Wood Mackenzie (Figure 1), we can see that Northeast production (blue line) began exceeding regional demand (purple area), seasonally at first and then year-round by the end of the last decade. The Northeast has been dependent on takeaway capacity ever since. Dozens of projects — primarily reversals and expansions of legacy pipelines — were completed in the 2014-19 period that allowed Appalachian gas supply to grow. However, there’s a long-running history of environmental opposition to new hydrocarbon infrastructure development in the region, and many projects were sidelined or canceled outright along the way. Moreover, just about all of the large-scale expansions that were planned or proposed have either been completed or canceled, and new projects to add significant takeaway capacity all but dried up. All in all, the appetite for capital investment in hydrocarbons development in the Northeast largely evaporated, particularly in light of the legal challenges and expensive delays faced by past projects. While at one point large-scale pipeline projects were able to move forward, that’s now far from a given.

Producers got some good news this summer: after a series of long and expensive legal battles, the last remaining tranche of large-scale pipeline capacity, Equitrans’s 2-Bcf/d Mountain Valley Pipeline (MVP) project, resumed construction, and the operator is targeting completion by the end of 2023. However, it took nothing short of an Act of Congress — i.e., the Fiscal Responsibility Act, which mandated and expedited completion of MVP — along with an emergency appeal to the Supreme Court and a favorable ruling from Chief Justice John Roberts to clear a path for MVP. Additionally, as we noted in our Bring It on Home blogs, when it does come online MVP won’t instantly translate to incremental production out of Appalachia, or for that matter, full utilization of the new pipeline capacity, despite the project being fully subscribed. That’s because, while there’s growing demand downstream of MVP, there are bottlenecks to get gas from MVP’s terminus at an interconnect with Williams’s Transco Pipeline to where it’s needed the most. (As we detailed in that blog series, Williams is undertaking a number of brownfield projects to expand capacity on the existing system to debottleneck deliveries into the New York area as well as to growing power markets in the Carolinas.) The other hitch is that while MVP and the related downstream expansions will allow regional production to grow by as much as 2 Bcf/d, without ongoing takeaway capacity additions producers will eventually grow into MVP and end up right back at square one — constrained.

As for other potential incremental outflow capacity, Equitrans’s Ohio Valley Connector Expansion (OVCX) is under construction and will add 350 MMcf/d on the existing OVC system via delivery to the Rockies Express (REX) and Rover takeaway pipelines. Other major takeaway pipelines, including REX and NEXUS Pipeline, are also considering brownfield expansions. Most recently, Enbridge said at its fall customer meeting that it is developing two projects that could expand its capacity to move gas west and south on its Texas Eastern Transmission (TETCO) system: Project Sparrow, which would offer up to 400 MMcf/d from TETCO’s M2 hub in southwestern Pennsylvania to interconnects with REX, Rover, and NEXUS at Clarington, OH; and a 1-Bcf/d brownfield expansion of TETCO’s 30-inch segment from Appalachia to Kosciusko, MS. Additional expansions like these, if they cross the finish line, would allow producers more room to grow. For now, however, after MVP, there are no other large-scale projects that are under construction, or even approved, that would increase takeaway capacity from Appalachia to markets outside the Northeast.

Given that bleak outlook for new egress out of the region, coupled with the reality of the wide seasonal demand swings that occur in the region, Appalachian gas producers have adopted a new playbook: using short-term mechanisms like throttling well completions and choke-management programs to avoid hitting the takeaway capacity wall and crushing supply-basin prices during low-demand periods, while still maintaining sufficient drilling activity to be able to respond when demand and prices improve.

Put another way, the big producers, including EQT, Antero and Southwestern, to name a few, have learned the cadence of drilling and building inventory when local demand is low and then turning their wells online to produce when demand is high. What’s more, they have become less willing to overrun what capacity they have. The “drill, baby, drill” sentiment of much of the Shale Era has been supplanted by the need to keep a floor under prices in a world where producers can’t count on new pipeline capacity to support growth — which means curtailing volumes, delaying completions, and making “game-time decisions” during times when takeaway capacity is at risk of filling up.

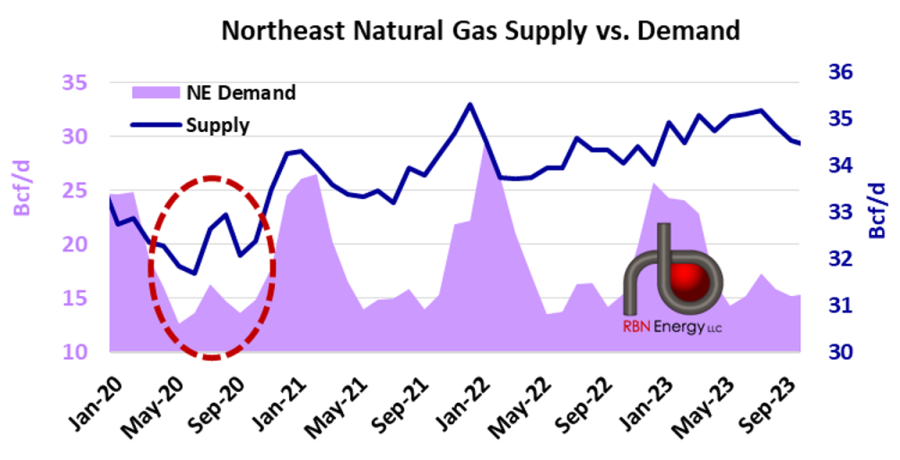

Figure 2. Northeast Natural Gas Supply vs. Demand. Source: RBN NATGAS Appalachia

We saw them employ that strategy for the first time in 2020 when the COVID-related shutdowns killed domestic and export demand (dashed red oval in Figure 2; see Flick of the Switch). And we’ve seen them employ it since then, albeit more subtly. (The volumes in Figure 2 show modeled supply and demand data from the RBN NATGAS Appalachia report.) Despite supply-basin prices rocketing to $9/MMBtu in 2022 and averaging more than $5/MMBtu for the full year — the highest in the Shale Era, according to daily pricing data from Natural Gas Intelligence (NGI) — production only rose an average 0.2 Bcf/d last year. We’ve also seen production pull back at times during the spring and fall shoulder seasons when demand troughs and pipeline maintenance intermittently reduce outbound capacity, or when Cove Point LNG conducts annual maintenance, which reduces in-region demand. Moreover, even with MVP now expected to come online, several producers said they were not planning to grow production into that new capacity, given the bottlenecks that exist downstream of MVP.

That’s quite a profound shift from historical producer behavior and has major implications for gas flow patterns and pricing. As producers increasingly respond to short-term price signals and make “game-time decisions” at the wellhead to optimize inventory — for example, by choking back in the shoulder months and ramping up during the winter when in-region demand peaks — we could see production take on a more seasonal pattern. Wintertime production would rise, eventually filling more of the pipeline capacity during the winter the way it normally does in the lower-demand shoulder months. Of course, ramping up production activity enough to balance against the high demand and ample exit capacity of the winter months means that producers would need to throttle wells during the shoulder and summer months to balance against lower demand and tighter exit capacity during those periods. In other words, we won’t see producers drilling blindly and blowing through the capacity wall in the shoulder months.

What this new reality entails for prices in the supply basin is that as supply becomes more seasonal, we would expect prices to become less seasonal, with increased supply in the winter dampening the price spikes and reduced supply in the lower-demand months creating a floor for prices.

Figure 3. Eastern Gas South Cash Basis History & RBN Forecast. Sources: RBN, NGI, Bloomberg

Figure 3 plots cash basis (regional differential to benchmark Henry Hub) at Appalachia’s Eastern Gas South (EGS) hub in $/MMBtu on the right axis, including daily basis history based on the NGI price index (solid blue line), forwards basis courtesy of Bloomberg (dashed blue line), and our EGS basis forecast (dashed purple line). The red line represents spare exit capacity in Bcf/d (left axis) — the takeaway capacity left over after outflows. When spare exit capacity dwindled to less than 2 Bcf/d in the fall of 2016-17, EGS cash basis plummeted to more than a $2/MMBtu discount to Henry Hub. Things improved in 2018-19 as a slew of pipeline projects were completed, adding more outbound pipeline capacity and easing constraints.

However, as the right side of the graph shows, we wouldn’t expect basis to weaken to the levels seen in 2016-17, even as spare exit capacity tightens year-round in the coming years. As producers manage their output seasonally to avoid severe constraint-driven basis discounts, we would expect the shoulder troughs not to fall quite as low as they have historically during low-demand periods. At the same time, winter basis would trend downward as pipelines fill up and Henry Hub rises. Restraint in the lower-demand periods and increased production in the higher-demand periods will mean a more rangebound forward curve. At the same time, overall tighter balances will create the potential for increased volatility during surprise, extreme weather events.

This blog was based on a presentation discussing our latest analysis of Appalachia gas fundamentals from our recent two-day School of Energy conference. We recorded all 16-plus hours of content, so you can watch each of the modules and run the accompanying lab model spreadsheets at your own pace. Want more information on the course content? Click here.

“We Can Work It Out” was written by Paul McCartney and John Lennon. It appeared as a double A-side single backed with “Day Tripper” that was released in December 1965. It went to #1 on the Billboard Hot 100 Singles chart and has been certified Gold by the Recording Industry Association of America. The song was recorded in two takes at EMI studios in London during the sessions for the Rubber Soul album. It was earmarked to be the non-album double A-side single to be released at the same time as the LP. A promotional film of the song with The Beatles was shot at Twickenham Film Studios in London with Joe McGrath directing. Personnel on the record were: Paul McCartney (lead vocal, acoustic guitar), John Lennon (Mamborg harmonium, bass, backing vocals), George Harrison (acoustic guitar, backing vocals), and Ringo Star (drums, percussion).

Rubber Soul was the album The Beatles were working on during the recording of “We Can Work It Out” and “Day Tripper.” Recorded between October-November 1965 at EMI studios in London with George Martin producing, it was The Beatles’ sixth studio album. Released in December 1965, it went to #1 on the Billboard 200 Albums chart and has been certified 6x Platinum by the RIAA.

The Beatles were an English rock band formed in Liverpool in 1960. Consisting of John Lennon, Paul McCartney, George Harrison, and Ringo Starr, they are regarded as the most influential band of all time. They released 17 studio albums, five live albums, 51 compilation albums, 36 EPs, and 63 singles. They have sold over 600 million records worldwide, making them the best-selling music act of all time. They are members of the Order of the British Empire (MBE), the Rock and Roll Hall of Fame, UK Music Hall of Fame, Vocal Group Hall of Fame, and have won one Academy Award, seven Grammy Awards, a Grammy Lifetime Achievement Award, 15 Ivor Novello Awards, one MTV Video Music Award, and three World Music Awards. Paul McCartney was knighted by Queen Elizabeth II in 1997. After the group’s breakup in 1970, all four band members went on to successful solo careers. John Lennon was murdered in December 1980. George Harrison died in November 2001. McCartney and Starr continue to record and tour as solo artists. There is rumor of a new Beatles track being released: a 1978 John Lennon composition called “Now and Then” being recreated by Paul McCartney using artificial intelligence to include all four of The Beatles on it. It is unknown if George Harrison’s “Sue Me, Sue You Blues” will be the flip side.